Certain Barclays Cards Now Offer Members Access to FICO Credit Scores

Barclaycard has just announced a positive change. FICO has made an agreement with Barclays to offer its members free access to its credit score results. Keeping on top of your credit is very important not only to qualify for top credit cards, but also in life. These are taken into account when you apply for apartments, mortgages or any kind of loans. Previously, getting a regular credit score from FICO would cost either $19.95 a month or would be available through a trial offer.

Although each agency Experian, Equifax and TransUnion uses a slightly different credit model, Barclays will provide the Transunion FICO score. That’s the one it tends to use. Although the three scores are not exact and this is not your official credit score, it’s a very good indication of everyone’s credit.

The score will update about every 60 days, which is still a useful time interval to monitor your credit. They will also offer:

- E-mail alerts triggered by changes in the score

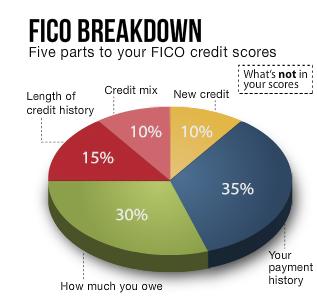

- Analysis of top factors impacting your score.

- Historical trends starting with 3 months of history and available for the past year.

To start receiving the free FICO credit score, Barclaycard members simply need to Log into their Accounts and accept the terms.

While this feature will roll out to more Barclays credit cards in the coming months or years, it’s currently available with Barclaycard Arrival, Frontier Airlines, Carnival, Barclaycard Ring, Barclaycard Rewards, and Juniper cards. Having free access to your FICO score is a nice perk, but not sufficient to make a credit card sign-up worth it. Many of the cards that currently offer the FICO score are not overly attractive otherwise, in my opinion.

However, the one credit card that I do like is the Barclaycard Arrival World MasterCard and this happens to be one of my favorite cards. It currently comes with a $440 sign-up bonus after spending $1000 within 3 months. You then continue to earn 2 miles per dollar for all spending on the card, making it essentially a 2.2% cash back card where the credit can be used for any travel purchase. That includes airline tickets, hotels, car rentals, train tickets, meals at hotels, etc. I am a big fan of this card as it really lets me pay for expenses that aren’t available with miles or where miles don’t offer good value. It’s a great card to just buy inexpensive domestic tickets.

Like this post? Join 700+ readers who subscribe to our blog posts by email and never miss another update or great miles deal. You can also follow us on Facebook or Twitter.

Would you use the Arrival Card or the AMEX SPG for non-multiple-points spends?

Those are definitely the two cards I tend to use and it’s really a tie! It depends on how many SPG points I have; if I need some, I’ll favor the SPG card. But if I have enough, I use Barclays since those points are always getting spent, even on taxi rides in NYC :)

Thanks for the 60 day mention. Was wondering why my FICO date for the Arrival card is showing 9/15/13 on Barclay site when I accessed it a couple days ago. At least they put the date so you know. I’ll check again in a few days and maybe it will be updated like you hinted.

Just an update. New FICO score effective 11/14/13 showed up. So the 60 days is right on. Went from 809 to 800. I’m doing something wrong. LOL.

Haha. Well, good to hear you have the most up to date 800+ number you possibly can!

It’s great that a card with decent rewards is finally offering a free score, walmart’s been doing it for years but their card is terrible.

Thanks for the great post!! I have the Barclaycard, logged in after reading your post to see if I could access my credit score. Success!! Thank you!!